The One Time Everything Falls Together

Why cash and short-term T-bills are the only things that hold when everything sells off at once.

Most investors know what a bear market looks like. Stocks go down, you hold on, and eventually things recover. It is uncomfortable, but it follows a logic you can reason through.

A liquidity crisis is something different. It does not follow that logic. It is the moment when investors stop asking “is this cheap enough to buy?” and start asking “what can I sell right now?” Everything becomes about raising cash, and it happens fast.

March 2020 was one of the clearest examples in recent memory. Within a matter of days, stocks collapsed. Fine, expected. But then gold sold off. Oil cratered. Bitcoin lost nearly half its value in a single trading day. Even US Treasury bonds, which had spent decades being the go-to panic buy for institutional investors, were being dumped. The yields on long-dated Treasuries actually rose during the worst of it, which is the opposite of what they are supposed to do during a crisis.

The reason comes down to one word: leverage. When you borrow money to hold positions, and those positions start falling, your broker does not wait around. Margin calls go out. Redemptions come in. Hedge funds running basis trades between Treasury futures and cash bonds found themselves forced to unwind everything at once, regardless of whether those positions were profitable or not. You sell what you can, not what you want to.

In that environment, gold is not a safe haven. It is just another asset with a bid price.

What the data actually showed

On the ten worst days for the S&P 500 during the COVID crash, short-term T-bills posted positive returns every single time. Not seven out of ten. Not nine. Ten out of ten. Gold, by comparison, fell on seven of those same ten days. Silver was even worse.

Why short-term T-bills specifically

Before getting into why they held up, it helps to understand what T-bills actually are. A Treasury bill is short-term debt issued by the US government, with maturities ranging from four weeks to one year. You are not earning a coupon like with a regular bond. Instead you buy the bill at a slight discount and receive the full face value back when it matures. The difference between what you paid and what you get back is your return. Because the US government is the issuer and the maturity is so short, there is almost no price risk. You know exactly what you are getting back, and you are not waiting long to get it.

This is where people often get confused. The US government issues three types of debt: T-bills (under one year), T-notes (two to ten years), and T-bonds (twenty to thirty years). Financial media lumps all three together as “Treasuries” or “bonds”, which makes it sound like they all behave the same way. They do not.

Long-dated bonds carry duration risk. Their price moves inversely with interest rates, and during a full-blown liquidity crisis those prices can move violently. Hedge funds also use long-dated Treasuries as collateral, which means when they need to raise cash fast, those bonds are among the first things they sell. In March 2020, foreign investors sold more than $300 billion worth of long-dated Treasuries. The Federal Reserve had to step in and buy $360 billion worth in a single week just to stabilize the market.

T-bills are a completely different story. They mature in weeks or months, so there is almost no duration risk. The price barely moves. They are as close to cash as you can get while still earning a yield. During a crisis that stability is exactly what institutions want, which is why the buying pressure on T-bills was so overwhelming in March 2020 while long bonds were being dumped.

The dollar factor

One layer that makes this even more interesting is what happens to the US dollar itself during a global liquidity squeeze. The dollar is the world’s reserve currency. Central banks hold roughly 60% of their foreign exchange reserves in dollars. More importantly, a huge portion of global debt, particularly in emerging markets, is denominated in dollars. When those borrowers need to pay down debt or post collateral, they need dollars specifically.

This creates a reflexive dynamic. As a crisis intensifies, demand for dollars rises globally, pushing the dollar index higher, which makes dollar-denominated assets relatively more attractive, which pushes more capital into cash and short-term US instruments. You saw this clearly in both 2008 and 2020.

It is worth noting that this dynamic is being questioned in a way it was not before. Since 2025, there has been growing concern among institutional strategists about whether US Treasuries will continue to play this role. Tariff uncertainty, a rising US fiscal deficit, and heavy Treasury issuance have made some investors rethink whether the dollar and short-dated US paper are as automatic a safe haven as they once were. That does not mean T-bills stop working tomorrow, but it is a real structural question worth watching.

Short-term T-bills are a different animal. They mature in weeks or months. There is almost no duration risk. The price barely moves. They are as close to cash as you can get while still earning a yield. During a crisis, that stability is exactly what institutions want, which is why the buying pressure on T-bills was so overwhelming in March 2020.

What to actually do with this

Before getting into the options below, the usual disclaimer applies: this is not financial advice, and everyone's situation is different. What follows are just some ideas worth exploring for parking short-term cash during a bear market. Do your own due diligence, check what is available in your country, and talk to a professional if you are unsure. With that said, most articles stop at the theory and leave you with nothing practical, so here are a few options worth knowing about depending on where you are and how you want to hold your cash.

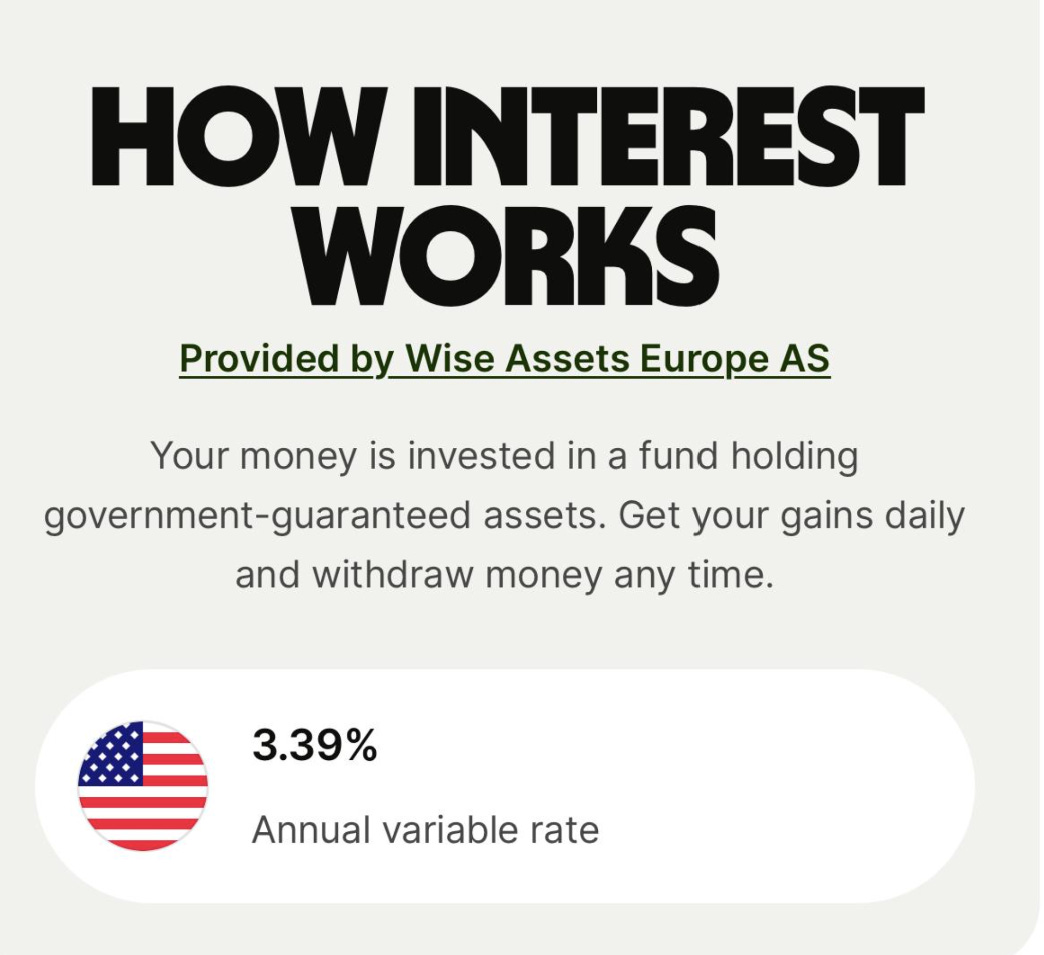

One option that has become genuinely useful for Europeans is Wise. If you open a Wise account and hold USD in it, you can enable their Interest feature, which invests your balance in a BlackRock short-term US government money market fund. As of mid-2026, that pays 3.39% annually on USD balances after fees, with no lock-up, no minimum, and daily accrual.

The underlying fund rate is 3.67%, and Wise takes 0.28% in annual fees, giving you the 3.39% net. You can send and spend your money at any time. The fund is the BlackRock ICS US Treasury Fund, so the underlying exposure is short-term US government paper.

The catch for Europeans is that you are converting euros to dollars, which introduces currency risk. If the dollar weakens against the euro, the exchange rate move can eat into your yield. That said, during a liquidity crisis specifically, the dollar tends to strengthen, so for the exact scenario this article is about, holding USD is actually a double benefit: you earn the yield and you get the dollar appreciation on top.

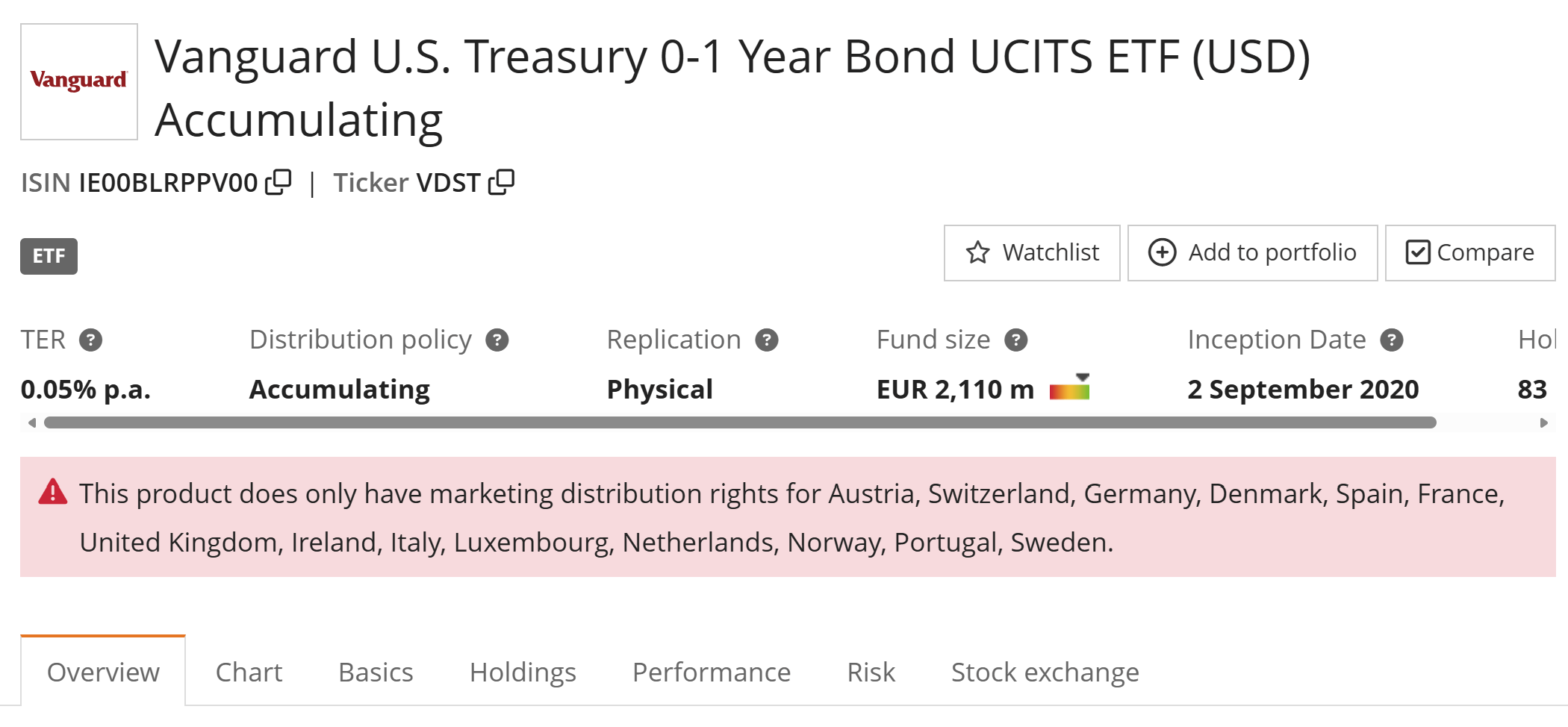

Another option Europeans could look into is getting T-bill exposure through an ETF. The Vanguard U.S. Treasury 0-1 Year Bond UCITS ETF (ticker: VDST, ISIN: IE00BLRPPV00) is one worth knowing about. The name is a bit confusing because it says "bond", but that is just Vanguard's generic label for fixed income. What matters is the 0-1 year maturity range, which means the fund only holds US government debt maturing within one year. The annual fee is 0.05%, which is negligible. You are not holding T-bills directly, but for a European retail investor without a US brokerage account, this is about as close as it gets.

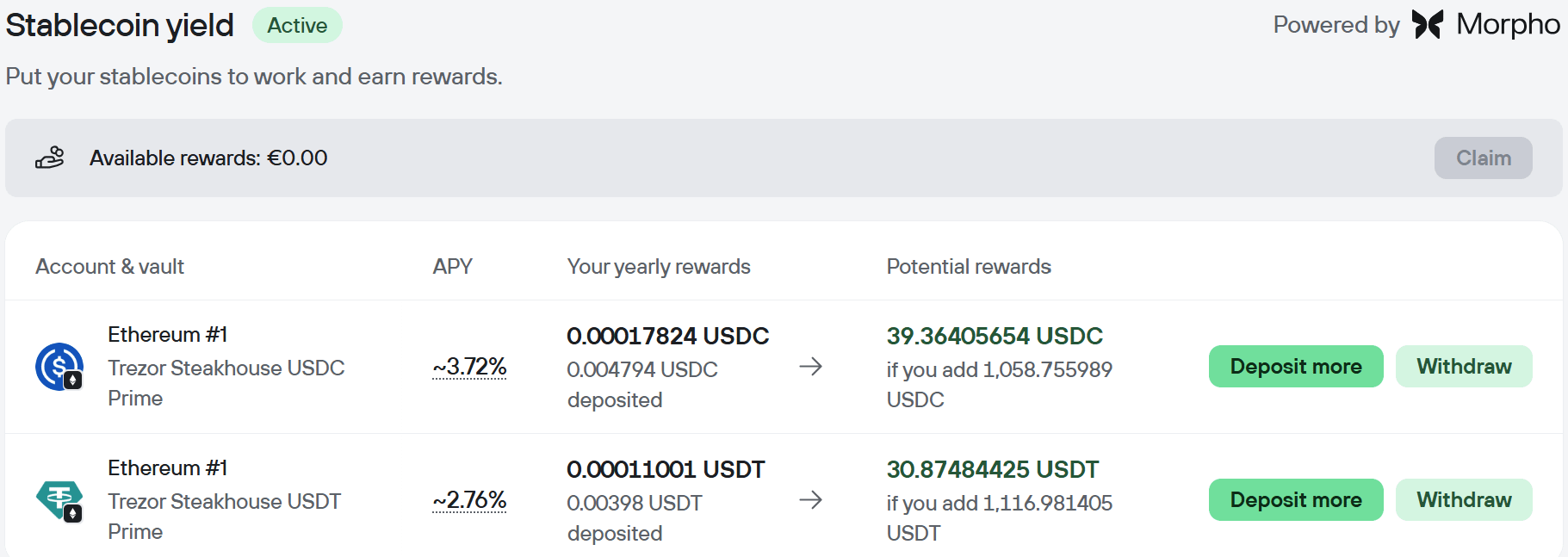

If you are already in crypto, there is a third option worth knowing about. USDC and USDT are dollar-pegged stablecoins that track the USD one for one. The advantage is that you can put them to work earning yield without touching a bank or a broker at all. Here is an example:

Final thoughts

Most people find out what a liquidity crisis feels like for the first time when they are already in one. The assets they thought were safe are down, the ones they thought were risky are down more, and everything is moving in the same direction at once. In those moments there is an old saying that proves itself over and over again: cash is king. And during a bear market, T-bills sit right next to it on the throne. They do not go up. They are not exciting. But they do not need a buyer on the other side to hold their value, and when everything else does, that boring quality becomes the most valuable thing in your portfolio.

As always, none of this is financial advice. Every situation is different, and what works for one person may not work for another. Do your own research, know your risk tolerance, and if in doubt talk to a professional. This is just one way of looking at it..